Monthly Market Update April 2026

Stay informed with the latest news and insights from Oxonian Capital's Monthly Market Update.

April 2026 Update:

MARKET NEWS

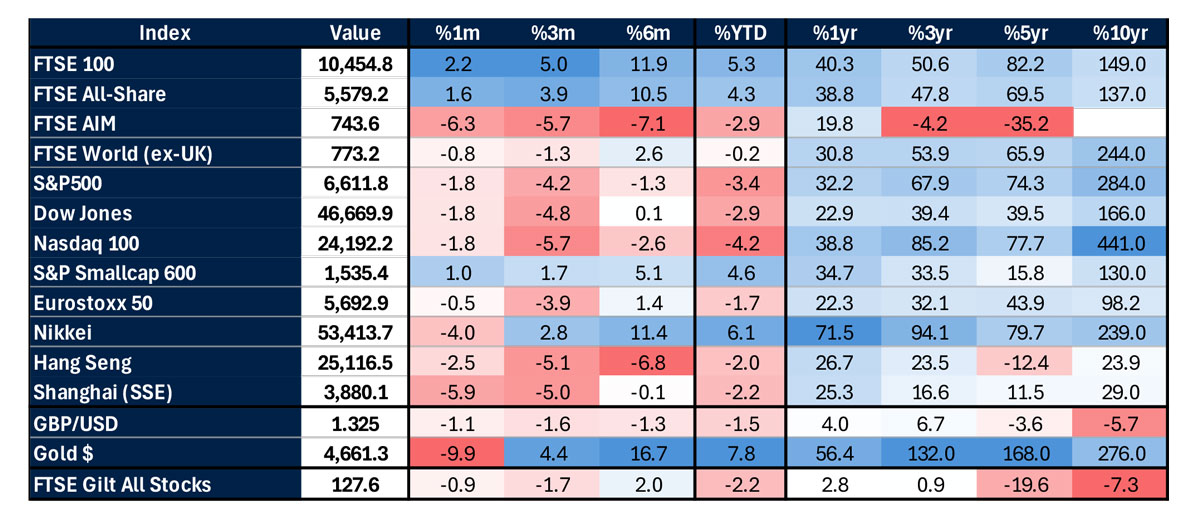

EQUITIES: Global equities suffered losses as the escalation of conflict in Iran triggered a selloff across most asset classes. The S&P 500 fell by -5.0%, while the European decline was more pronounced, with the STOXX 600 falling -7.5%, its worst monthly performance since 2022. The FTSE 100 fell -6.2%, despite a heavy weighting to energy names in the index. U.S. tech shares were also weaker, with the NASDAQ falling -4.7%, though outperforming most major indices as large‑cap stocks provided some resilience after earlier declines in software names.

Markets that had performed strongly early in 2026 saw pronounced reversals. The MSCI Emerging Markets index declined -13% in March, while Japan’s Nikkei fell -12.7%. Despite this, Japan remained positive year‑to‑date (+2.1%), with Emerging Markets broadly flat (-0.1%), both outperforming global equities overall (-3.1%). Brazil’s Bovespa is also worth comment, having risen +16.3% this year, and a fall of just -0.7% in March, providing investors with good diversification, albeit not without risks.

CURRENCY: The U.S. Dollar regained its status as the world’s primary safe haven, with the dollar index strengthening +2.4% in March as investors fled toward ‘safe’ liquidity. The Pound faced pressure as a result, slipping to $1.324 at the end of the month. This represented a fall of -1.9%, exacerbated by a combination of rising unemployment and cooling wage growth, leading some to speculate on an earlier-than-expected intervention by the Bank of England to support growth, despite the inflationary spike. The Euro fared slightly worse, due to the economy’s reliance on imported gas, with the currency falling -2.2% against the Dollar.

BONDS: Bond markets were impacted by a sharp repricing of inflation expectations. 10-year U.S. Treasury yields rose by +0.38% in March to end at 4.32%, the biggest monthly jump since December 2024. In Europe, 10-year Bund yields rose to 3.01%, marking the first time since 2011 that they have closed above 3%. In the U.K., Gilts also suffered, with yields rising +0.63% for the 10-year, closing the month at 4.87%. Short-term expectations for interest rates shifted dramatically; at the start of the quarter, futures priced in 0.61% of U.S. interest rate cuts for 2026, but by the end of March, this had fallen to just 0.07%. Index-linked bonds offered some protection but still saw capital declines as inflation expectations were reset given the oil price shock.

ALTERNATIVES: Energy markets dominated returns. Brent crude oil surged +51.3% in March, closing at $118.35. The move pushed the market into backwardation, with 6‑month forward prices ending the month at $82.95, suggesting expectations are that supply disruption will ease over time. Gold failed to provide its traditional protection, falling -11.6% – its largest monthly decline since October 2008 – as a stronger Dollar and higher real yields undermined its appeal.

MACRO NEWS

POLITICS: The geopolitical landscape underwent a seismic shift in March as tensions in the Middle East finally boiled over. The conflict in Iran – marked by targeted strikes on enrichment facilities and the threat of mines in the Strait of Hormuz – has effectively removed a primary artery of global trade. Approximately 21 million barrels of oil per day, or roughly 20% of global consumption, is currently contested or blocked.

The political fallout has been immediate, and we have seen a fracture in geopolitical consensus, with Washington and London committed to reopening the Strait, but Beijing maintaining neutrality and securing land-based energy deals with Russia and Central Asian countries. For the U.K. and Europe, this necessitates a rapid reassessment of future economic strategy.

As we go to press, we note the two-week ceasefire agreed between Iran and the U.S. Unsurprisingly, this has seen the oil price fall sharply, and rallies in global equity and bond markets

MONETARY POLICY: Central bankers find themselves trapped in a policy “pincer movement” that evokes the stagflationary ghosts of the 1970s. The Bank of England (BoE) and the Federal Reserve began March expecting to discuss the timing of interest rate cuts, but they ended it defending the necessity of holding rates or even hiking.

At the March meeting of Federal Open Market Committee, Chairman Jerome Powell acknowledged that the 50% spike in energy prices acts as a regressive tax on consumers, which would typically be deflationary for growth. However, the second-round effects on transportation and manufacturing costs have sent 5-year inflation breakeven rates (a key market gauge of future inflation) to their highest levels since the 2022 energy crisis.

In the U.K., the BoE is in an even tighter spot. With the economy showing signs of fatigue, Governor Andrew Bailey faces the unenviable task of curbing imported inflation without triggering a recession. The market is currently pricing in a wait and see approach for the upcoming meetings, but the “Goldilocks” scenario of 2025 has been replaced by a concerns of stagflation.

ENERGY SECURITY: The most pressing macro theme remains the permanence of the energy price shift. U.K. Natural Gas prices for Summer 2026 rose by 79% in March and the forward curve for gas has seen the seasonal discount effectively vanish. This means summer gas is now trading at almost the same premium as winter gas. This reflects a fundamental fear that European storage (currently at 28%) will be impossible to refill to the 80% target by November without the usual flow of Qatari LNG, which has been hampered by events in the Persian Gulf. For investors, the “energy transition” may be shifting from a long-term ESG goal to an immediate, national security priority.

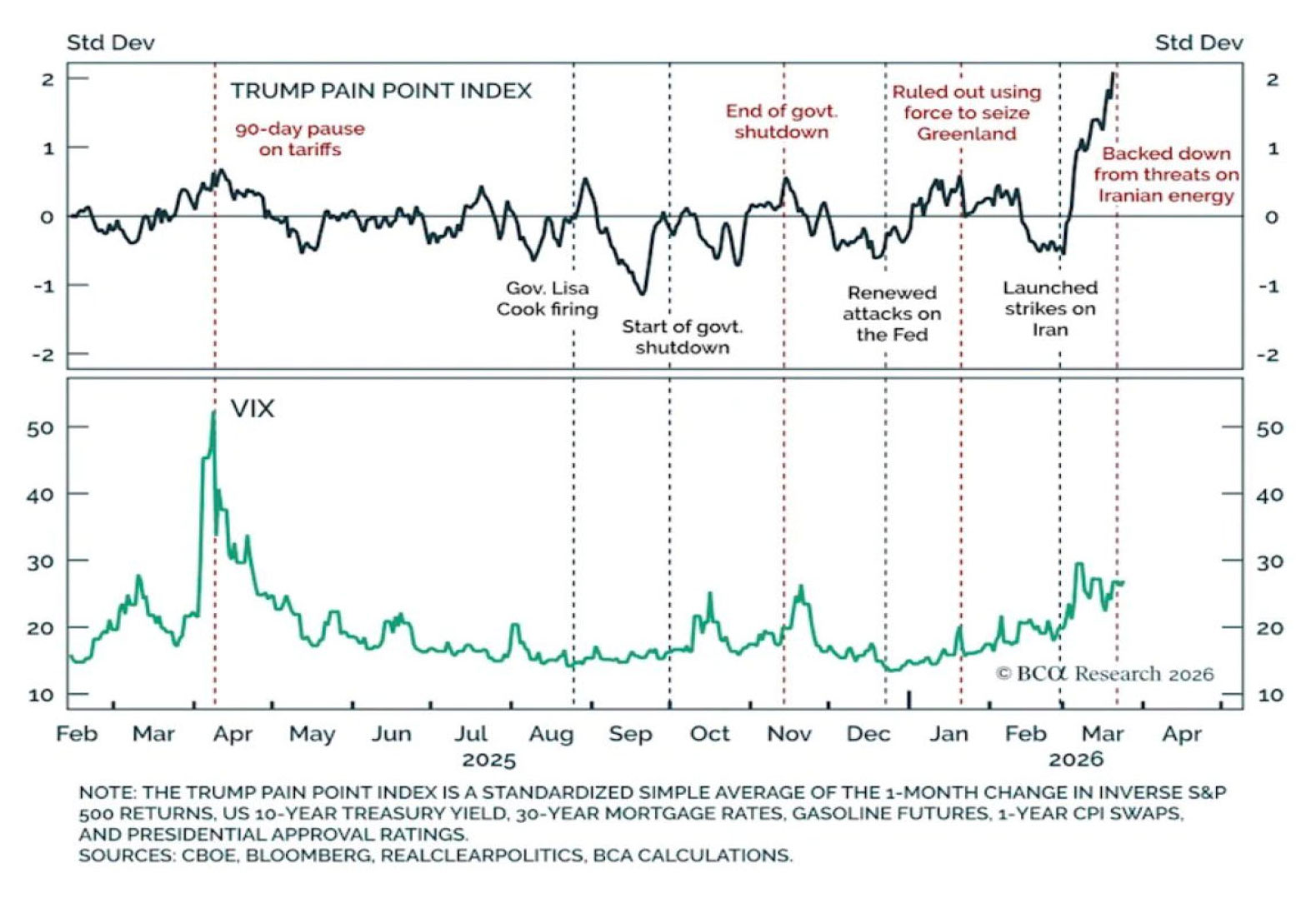

CHART OF THE MONTH

BCA Research have developed a TACO (Trump Always Chickens Out) indicator showing how much pain markets are causing President Trump, and when he might back down. That indicator reached a new high last week and, despite the two-week ceasefire announced just prior to publication, it remains to be seen how negotiations with Iran progress. So far at least, markets have taken the news of a ceasefire in their stride, and the below ‘pain point’ is likely easing for the President.

Source: BCA Research. Available at: https://www.bcaresearch.com/reports/quantifying-tacos-24-03-2026/213941

MARKET DATA

Source: Alpha: data as at 07-04-26 intra-day prices