Monthly Market Update July 2026

Stay informed with the latest news and insights from Oxonian Capital's Monthly Market Update.

July 2026 Update:

MARKET NEWS

EQUITIES: European equities continued higher, with the Stoxx 600 index up +2.7% led by financials (+6.4%). The U.S. picture was more nuanced, with the S&P 500 slipping -1.0% and the Nasdaq -2.7%, even as financials rallied (+4.4%) as the Fed pivoted on rates. The Philly Semiconductor Index climbed a further +11% (now +102% YTD). Asia was volatile, with the Hang Seng down -8.5%, while South Korea's Kospi index, up +102.4% YTD, ended flat having been up over +7.5% intra-month. Japan's Nikkei added +5.7%, taking its half-year return to +40.4%, aided by yen weakness. Emerging markets were softer, with the MSCI EM index down -1.4%.

Markets have rotated from the Mag-7 (-2% YTD) and gold, toward AI-enabling semiconductors and more cyclical areas like financials. We share the market's growing caution around the scale of moves in the AI space – reminiscent of gold's earlier rally – and would favour a more selective stance from here.

CURRENCY: The dollar had its strongest month of the year, with the DXY up +2.3% as the Fed's repricing accelerated after Kevin Warsh's first meeting as Chair. Sterling fell -1.4% and the euro declined -2.0% against the dollar. The yen was the weakest major currency again, down -2.0% and at its lowest since 1986, despite a small BoJ rate rise to 1%. Commodity currencies also struggled, with the Australian dollar down -3.7%.

BONDS: Government bonds posted modest gains as the dust settled from the Iran conflict, though the tone remained cautious given the hawkish shift from several major central banks. UK Gilts returned +0.6% and Eurozone sovereigns added +0.5%. US Treasuries returned +0.4%. Corporate credit was broadly flat to modestly positive, with U.S. high yield returning +0.2% and European high yield +0.6% – unremarkable moves that mask a genuinely pivotal month for rate expectations, as markets moved decisively away from pricing further cuts in 2026.

Given record-low corporate-to-government bond spreads, we increased government bond exposure in June, partly funded by trimming corporate exposure at the index level. Again, we reiterate the need to be selective.

ALTERNATIVES: Commodities had a tough month. Brent fell -20.8% and WTI -20.4% as the naval blockade lifted, taking oil back to pre-conflict levels (but still +19.8% YTD). Gold fell -11.7% and silver -22.2% as easing geopolitical risk and rising rate expectations removed two key supports. Copper slipped -3.1%, and Bitcoin extended its run of quarterly declines. Gold now sits at the psychologically important $4,000/oz level – a break lower here could prove significant.

MACRO NEWS

POLITICS: June brought a resolution to the Iran conflict that had dominated markets since the spring. Early in the month, renewed strikes reignited tensions, and President Trump warned Iran would “pay the price” for delaying a deal, followed a day later by threats to take Kharg Island. That was then cancelled, and on 14th June Trump announced a ‘framework agreement’ with Iran was complete, lifting the U.S. naval blockade. The agreement was then signed, hopefully drawing a volatile period of diplomacy to a close.

Keir Starmer announced his resignation as prime minister on 22nd June, after sustained pressure post May's local election losses, and a string of Cabinet departures. Andy Burnham, who won the Makerfield by-election on 18th June, is the clear favourite to succeed him – with Wes Streeting and Angela Rayner both confirming they will back him. Starmer remains in post until a new leader is elected, with the contest concluding by 1st September at the latest – sooner if Burnham stands unopposed. We await with interest who the new chancellor will be, with Ed Miliband and Wes Streeting the front-runners.

MONETARY POLICY: Kevin Warsh's first meeting as Federal Reserve Chair on 17th June saw rates held, but the dot plot chart marked a sharp break from prior guidance. Half of participating policymakers projected at least one further rate increase in 2026, versus a single cut pencilled in as recently as March. In line with this, markets are currently pricing in at least one further rise for the rest of 2026. The ECB delivered its first rate increase since 2023, with President Lagarde describing the move as warranted, despite a milder inflation forecast. The Bank of Japan also increased rates though this did little to stop yen weakness. The Bank of England held rates at 3.75% for a fourth consecutive meeting, but two members voted for an immediate +0.25% rise, amid concerns of inflation caused by elevated energy prices.

SEMICONDUCTOR SUPPLY SHOCK: A supply squeeze in Q2 was driven by strong AI infrastructure demand and shortages across memory chips and storage. Apple raised iPad and Mac prices in response, while chip stocks rallied sharply. The Philly Semiconductor Index rose +11% in June and +88% in Q2, its best quarter since the early 1990s.

That said, semiconductor share prices have run well ahead of profit growth, increasing the risk of a correction if AI-related capex disappoints. Hyperscaler capex is still projected to rise 83% in 2025, which remains supportive, but with valuations at much loftier levels, expectations now leave little room for disappointment.

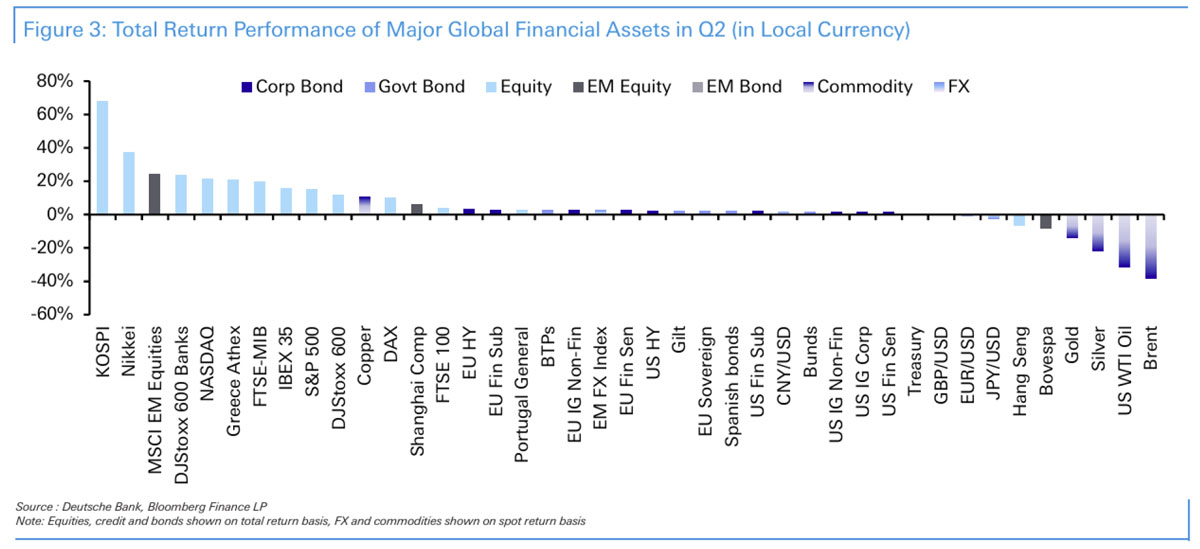

CHART OF THE MONTH

Having reached the half-way point of the year, it is natural we look at returns across asset classes so far in 2026. Helpfully, Deutsche Bank show this in their performance update, shown in the chart below. We have covered the Kospi and Nikkei already in this note, and the only real laggard in equity markets the Hang Seng in China with tech stocks out of favour in China and weaker domestic data causing concern. Copper is a key part of the AI revolution, thanks to its conductive qualities and whilst the price fell in June, it has now risen by more than 40% over the last 5 years – comparing favourably to other materials like aluminium (+22%). With gilts, it is easy to think of government uncertainty, inflation and concerns over spending leading to higher yields (lower prices), but they have had a solid quarter relatively speaking, up +2.1%, versus U.S. treasuries up +0.4% and German Bunds up +1.4%.

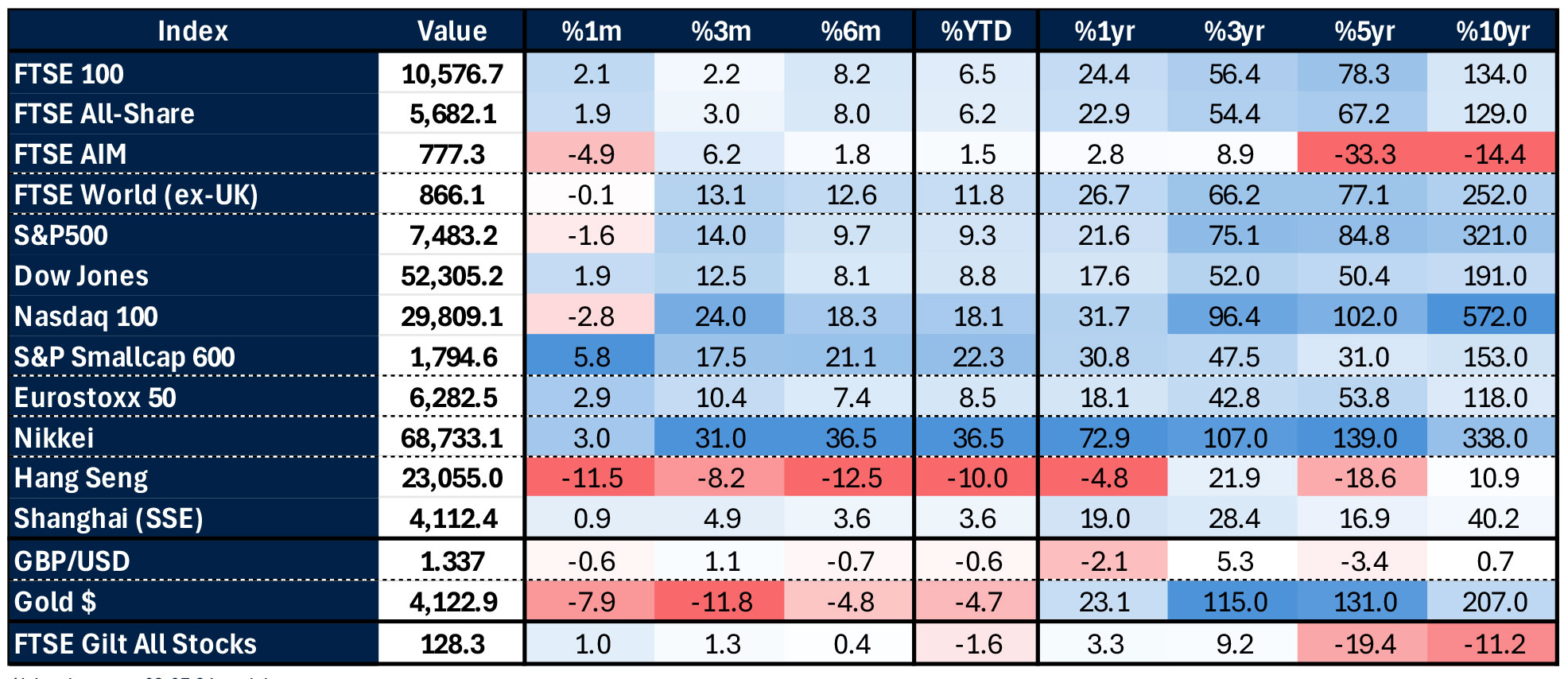

MARKET DATA

Source: Alpha: data as at 02-07-26, mid-day pricing